Per Diem Interest: Why Your Closing Date Matters

You've found the home, negotiated the contract, survived the inspection, and signed enough paperwork to qualify as a part-time attorney. Then your lender sends over the final numbers, and you notice a charge called per diem interest.

What is it? Why are you paying it? And can the day you close affect how much you owe?

The answer is yes.

While per diem interest isn't usually the biggest cost in a transaction, understanding how it works can help you better manage your cash at closing. In some cases, simply choosing a different closing date can save hundreds—or even thousands—of dollars upfront.

💰 What Is Per Diem Interest?

"Per diem" means "per day."

Mortgage interest starts accruing the day your loan funds. Since mortgage payments are paid in arrears, your lender collects the interest owed between your closing date and the end of that month at closing.

Think of it like joining a gym halfway through the month. You still pay for the days you're using the membership before the next billing cycle begins.

The same concept applies to your mortgage.

The calculation looks like this: Loan Amount × Interest Rate ÷ 365 = Daily Interest

Then: Daily Interest × Number of Days Remaining in the Month = Per Diem Interest Due at Closing

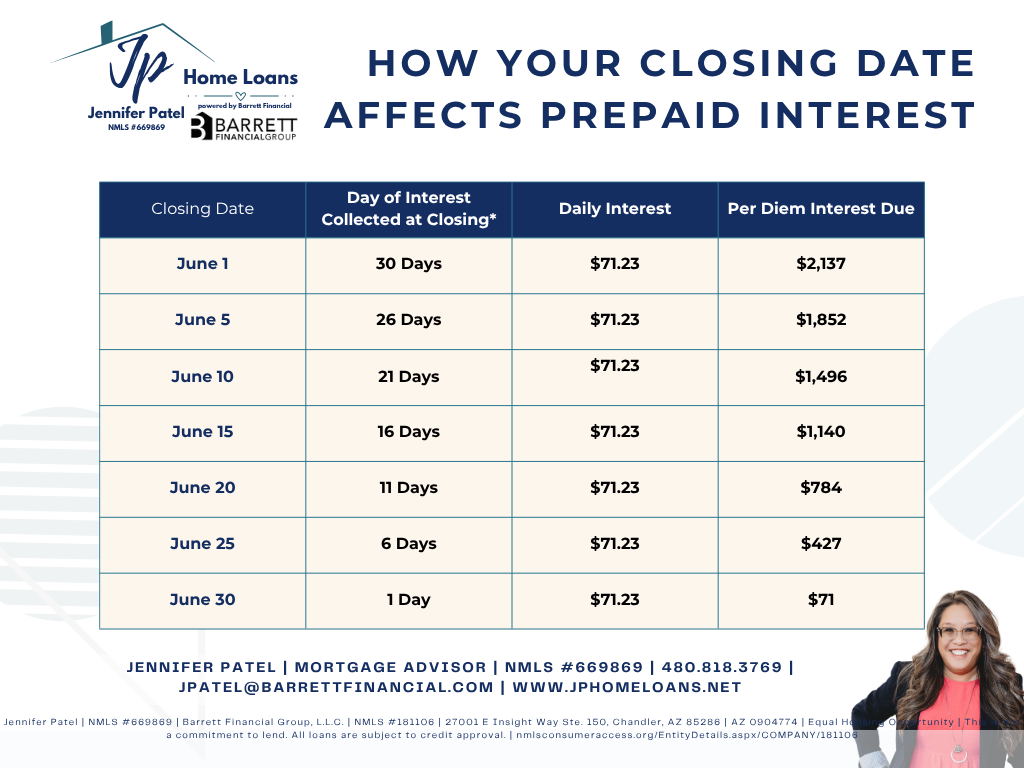

🧮 Let's Look at an Example

Let's assume:

Loan Amount: $400,000

Interest Rate: 6.50%

Daily interest would be:

$400,000 × 6.50% ÷ 365 = $71.23 per day

Now let's see how the closing date changes the amount of prepaid interest due at closing.

*Example assumes a $400,000 loan at 6.50% interest. Actual calculations may vary slightly based on lender methodology and the number of days in the month.

📊 What Does This Mean?

At first glance, it looks like closing on June 30 is the obvious winner. After all, paying $71 sounds much better than paying more than $2,000.

But here's the important part: you're not avoiding interest—you’re simply changing when you pay it.

Interest accrues every day your loan is active. Closing earlier in the month means you'll bring more prepaid interest to closing. Closing later means you'll bring less.

For borrowers trying to minimize their upfront cash requirements, a late-month closing can often be advantageous.

📅 When Is Your First Mortgage Payment Due?

Here's where things get even more interesting.

For most mortgages, your first payment is due on the first day of the second month after closing.

For example:

Close June 5 → First payment due August 1

Close June 25 → First payment due August 1

Notice both borrowers have the same first payment date.

The borrower who closed on June 5 prepaid significantly more interest at closing, while the borrower who closed on June 25 prepaid much less.

That's why many buyers and homeowners refinancing choose a closing date toward the end of the month whenever timing allows.

🏡 Does This Apply to Purchases and Refinances?

Yes.

Whether you're purchasing your first home, upgrading to a larger home, downsizing, or refinancing an existing mortgage, interest begins accruing when the loan funds.

The mechanics are exactly the same.

The difference is simply how much prepaid interest you'll need to bring to the closing table based on the day your transaction closes.

🌞 Why the "Best" Closing Date Depends on Your Goals

While closing near the end of the month often reduces prepaid interest, it isn't automatically the right choice for everyone.

Sometimes the best closing date is the one that:

Fits your moving schedule

Keeps your rate lock from expiring

Meets contractual deadlines

Coordinates with the sale of another property

Creates less stress for everyone involved

I've seen borrowers save a significant amount of cash by shifting their closing date by just a few days. I've also seen borrowers gladly pay a little more in prepaid interest because it made the entire transaction smoother.

Like most things in mortgage lending, context matters.

🐼 Mama Bear Tip

If you're trying to reduce your cash needed at closing, ask your lender to run estimates using a few different closing dates.

A simple adjustment of one week could leave several hundred dollars—or even more—in your pocket for moving expenses, furniture, or the inevitable Home Depot run that somehow turns into three Home Depot runs.

🤝 The Bottom Line

Per diem interest isn't a hidden fee or an extra charge from your lender. It's simply the interest that accrues between your closing date and the end of the month.

Because interest accrues daily, borrowers who close later in the month typically bring less prepaid interest to closing, which can lower their cash-to-close amount. However, the right closing date should always balance your financial goals, contract deadlines, and overall transaction timeline.

If you're buying a home or considering a refinance, I can help you compare different closing scenarios so you understand exactly how timing affects your numbers.

Ready to see how this could work for you? Contact me to start your next smart move toward homeownership.