Bridging the Down Payment Gap

Let’s be honest—saving for a down payment is one of the biggest hurdles to buying a home. If you’re feeling stuck between rising rents and rising home prices, I’ve got good news: you’ve got options, and I’m here to help. From down payment assistance grants to low down payment programs, we can create a strategy to get you into a home with less cash out of pocket than you might think.

Let’s dive into three powerful tools that are helping real people buy homes right now.

☀️ HOPER: Down Payment Assistance with a Solar Twist

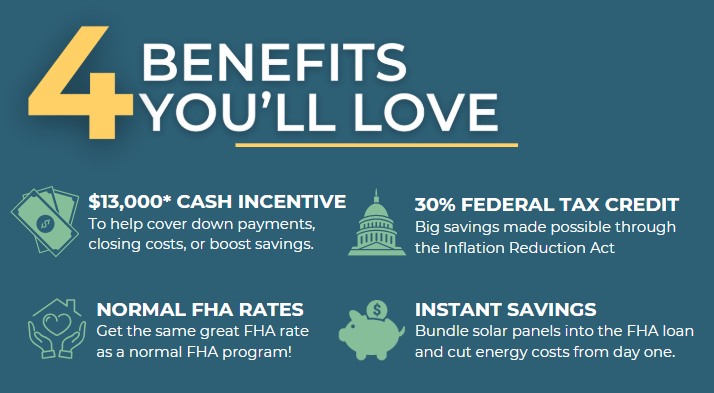

The HOPER program, administered by Attainable Housing Associates, is a fantastic option for Arizona buyers who want down payment help while also investing in long-term energy savings. But here's the key: to qualify, you must purchase a solar panel system as part of the home purchase and loan structure.

How it works:

Receive 3.5% of the purchase price, up to $13,000, in assistance

Assistance is taxable income, but does not need to be repaid

Must be paired with an FHA loan

Must purchase (not lease) and finance the solar panel system into the loan

Participation in a research program required:

Online financial education before going under contract

Financial mentorship after closing

Federal solar tax credit can help offset the tax liability if the system is installed prior to 12/31/2025. (talk to your tax advisor!)

So, why solar? Owning your system means lower utility bills, greater home equity, and long-term energy cost protection.

One of my clients in San Tan Valley used HOPER to buy her home and now has shrinking electric bills every month. 🌞

👉 Check out my🔗 previous blog post on HOPER for all the fine print and bonus info!

The Federal Tax credit is for systems installed prior to 12/25/2025.

💵 1% Down Payment Program: Big Help, Little Upfront

If solar isn’t your thing, this low down payment program is another great path to homeownership. It’s ideal for buyers with decent credit who want to keep more of their cash in the bank.

How it works:

You contribute just 1% of the purchase price

You receive up to $7,000 in assistance to complete the required 3% down payment

Must be used with a conventional loan

Available to first-time and repeat buyers

A recent client in Avondale had just $5,000 saved. With this program and some seller help, she closed on her new home with cash to spare.

Another couple in Mesa used it to move into their dream home and still had enough left for new furniture and moving expenses. 🎉

🏦 Traditional DPA Programs: Forgivable (and Some Repayable) Second Mortgages

If you need a little more flexibility or don’t want to go the solar route, there are several down payment assistance programs that offer 3.5% to 5% in the form of a second mortgage. These programs are available statewide and can be a game-changer for buyers who have steady income but not a lot saved for upfront costs.

Here’s what you should know:

Can be used with both FHA and conventional loans

Minimum credit scores as low as 580

Assistance typically comes in the form of a second mortgage

3.5% assistance programs are often forgivable after a set number of years (usually 3) if you stay in the home and meet the guidelines

⚠️ 5% assistance programs usually require repayment when you sell, refinance, or pay off the first mortgage—so it’s important to know which type you're getting

These programs come in a variety of formats: some forgive the loan after you meet the criteria, others require repayment under specific circumstances. I’ll help you understand the fine print so you can choose what works best for your financial future.

One of my recent clients used a forgivable 3.5% DPA loan and only needed to bring a few hundred dollars to closing. Another opted for a 5% repayable assistance program, which gave them more cash upfront and time to settle into their new home comfortably.

✅ Pros & Cons of Down Payment Assistance Programs

Pros:

Makes homeownership possible with less cash upfront

Options available for a wide range of credit scores and loan types

Programs like HOPER offer long-term financial education and mentorship

Solar and forgivable DPA options may offer utility or future loan savings

Cons:

Some assistance (like HOPER) is taxable

Programs may come with income limits, loan type restrictions, or education requirements

Assistance may be tied to specific conditions like solar purchase or longer ownership periods

🏡 Let’s Create Your Homebuying Plan

Whether you're leaning toward solar, keeping it simple with the 1% down option, or looking into forgivable DPA loans, I’m here to guide you through the process from start to finish.

📲 Call, text, or DM me today and let’s put together a custom plan that works for your budget and your goals.

And don’t forget to check out my HOPER deep-dive blog post on the website if you're curious about going solar and saving green in more ways than one!