🏡 Property Inspection Waivers:

Wait… You Might NOT Need an Appraisal?

If you’ve ever purchased a home or refinanced a mortgage, you’ve probably heard the word “appraisal” tossed around early in the process. For years, appraisals were considered a mandatory step in nearly every mortgage transaction.

But today?

That’s not always the case.

In certain situations, borrowers using conventional financing may qualify for what’s called a Property Inspection Waiver (PIW) — also commonly referred to as an appraisal waiver.

Before we get into how those work, let’s start with the basics.

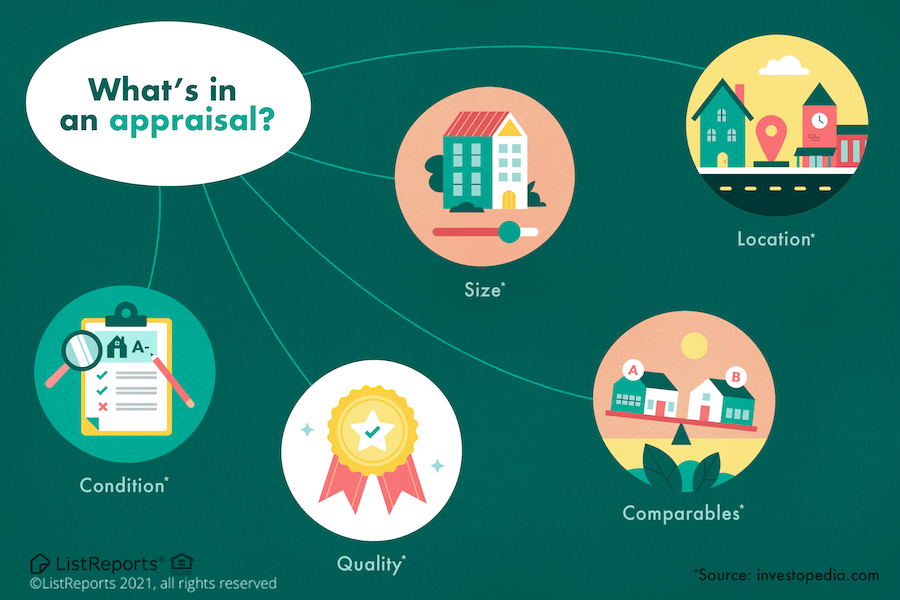

📊 What Is an Appraisal — And Why Does It Matter?

An appraisal is a professional opinion of a property’s market value completed by a licensed appraiser. The lender uses this report to confirm the home is worth what is being paid or refinanced.

After all, the property itself acts as collateral for the mortgage loan.

The appraisal helps protect:

The borrower

The lender

The stability of the overall housing market

A traditional appraisal typically includes:

A physical inspection of the property

Interior and exterior photos

Measurements and condition notes

Comparable nearby home sales

Market analysis

The goal is to determine whether the home supports the loan amount being requested.

And in many cases… it still does exactly that.

But technology and mortgage data systems have evolved dramatically over the years.

👀 What Is a Property Inspection Waiver?

A Property Inspection Waiver allows certain conventional loans to move forward without requiring a traditional appraisal inspection.

That means:

✅ No appraiser appointment

✅ No waiting on a full appraisal report

✅ No appraisal fee in many cases

✅ Potentially faster loan processing

Instead of requiring a physical inspection, automated underwriting systems through Fannie Mae or Freddie Mac analyze enormous amounts of existing property and market data.

These systems review:

Prior appraisal history

Public records

Comparable sales

Market trends

Loan-to-value ratios

Property characteristics

Borrower profile and overall risk

If the automated system determines there is sufficient reliable data available, it may offer the lender a waiver.

Translation?

The system is essentially saying:

“We already have enough confidence in this property value.”

🚨 Important: Appraisal Waivers Are ONLY for Conventional Loans

This is one of the biggest misconceptions in mortgage lending.

Property inspection waivers are generally available only for:

Conventional loans backed by Fannie Mae

Conventional loans backed by Freddie Mac

You typically will NOT see appraisal waivers available on:

FHA loans

VA loans

USDA loans

Government-backed loan programs usually require some level of physical appraisal because those loans also include minimum property condition requirements and safety standards.

So if someone tells you:

“My cousin skipped the appraisal on their FHA loan…”

…there’s a very good chance that’s not the full story. 😅

🏡 Other Types of Mortgage Appraisals

Not every appraisal looks the same. Depending on the loan program and scenario, several different valuation methods may be used.

Full Appraisal

The traditional appraisal with a full interior and exterior inspection.

Drive-By Appraisal

The appraiser views only the exterior of the property and completes the valuation using market data.

Hybrid Appraisal

A third-party inspector collects property information while the appraiser completes the valuation remotely.

Desktop Appraisal

Completed entirely remotely using available data sources.

Property Inspection Waiver

No appraisal inspection required at all if the automated system approves the waiver.

Each option depends on:

Loan type

Risk level

Equity position

Occupancy type

Property characteristics

Automated underwriting findings

⏰ Why This Matters for Buyers and Homeowners

If a conventional loan receives a property inspection waiver, it can create several advantages for borrowers.

Potential benefits may include:

Faster closing timelines

Reduced out-of-pocket costs

Less scheduling stress

Fewer delays during escrow

But it’s important to remember:

A waiver is never guaranteed.

Two borrowers purchasing similar homes may receive completely different appraisal requirements depending on the specifics of the file.

That’s why working with an experienced mortgage professional matters.

Understanding how to structure the loan properly from the beginning can help position the file for the best possible outcome.

🐼 Final Thoughts

The mortgage world is changing fast, and appraisal options are evolving right alongside it.

While traditional appraisals are still extremely common and important, many conventional borrowers today may qualify for alternative valuation methods — including desktop appraisals or even full property inspection waivers.

The key is understanding:

Which loan programs allow them

When they apply

And how the automated systems make those decisions

Every loan scenario is different, and having the right strategy can make a huge difference in both timing and overall experience.

If you’re thinking about buying, refinancing, or wondering whether your loan could qualify for an appraisal waiver, reach out to me directly. I’d be happy to review your options, answer your questions, and help build a game plan that fits your goals.

📩 Contact me today and let’s talk through your next move.