🏡Not All Credit Help Leads to Faster Homeownership

When buyers start preparing for a mortgage, one of the first things they focus on is improving their credit. That makes sense. Higher scores can mean better interest rates, lower monthly payments, and more loan options.

But this is also where many buyers accidentally take the wrong turn.

A lot of people assume all debt or credit programs work toward the same goal. In reality, some programs are built to help reduce financial strain long term, while others are specifically designed to improve a borrower’s mortgage profile as efficiently as possible.

And the difference can dramatically affect how quickly someone is able to buy a home.

Let’s look at a common example.

Imagine a young couple hoping to buy their first home. They have stable income, a qualifying credit score around 620, an auto loan, a few high credit card balances, and some lingering medical collections from a few years ago. They are financially hanging in there, but they know they need some help cleaning things up before applying for a mortgage.

Like most people, they head online and start researching solutions. That’s when they discover two very different paths: debt consolidation programs and credit optimization programs.

At first glance, they sound almost identical. But what happens next can look very different.

🔄 The Debt Consolidation Route

In the first scenario, the couple signs up with a debt consolidation company because the lower monthly payment sounds appealing. The company combines several debts into one structured repayment plan and begins negotiating with creditors. Some accounts are closed during the process, and the couple is advised to stop using certain credit cards altogether.

Initially, this can feel like a huge relief. Instead of juggling multiple due dates and interest rates, they now have a simpler monthly structure. Their financial stress may decrease, and their monthly budget may improve.

But from a mortgage standpoint, things can get more complicated.

As accounts close and negotiations begin, their credit scores may temporarily drop. Some lenders may view active debt management or settlement plans cautiously, especially if there were missed payments during negotiations. Even though the couple is technically improving their financial situation, their mortgage readiness may actually slow down in the short term.

Instead of buying in a few months, they may now need additional time for scores to recover and for underwriters to feel comfortable with the new credit profile.

That does not mean debt consolidation is “bad.” For many families dealing with overwhelming payments or serious hardship, it can be a lifesaver. But if the immediate goal is homeownership, borrowers need to understand that the timeline may be longer than expected.

📈 The Credit Optimization Route

Now let’s rewind and take the same couple in a different direction.

Instead of entering a consolidation program, they work with a mortgage-focused credit optimization company. Rather than restructuring debt, the focus is placed on strategically improving the factors that affect mortgage scoring models.

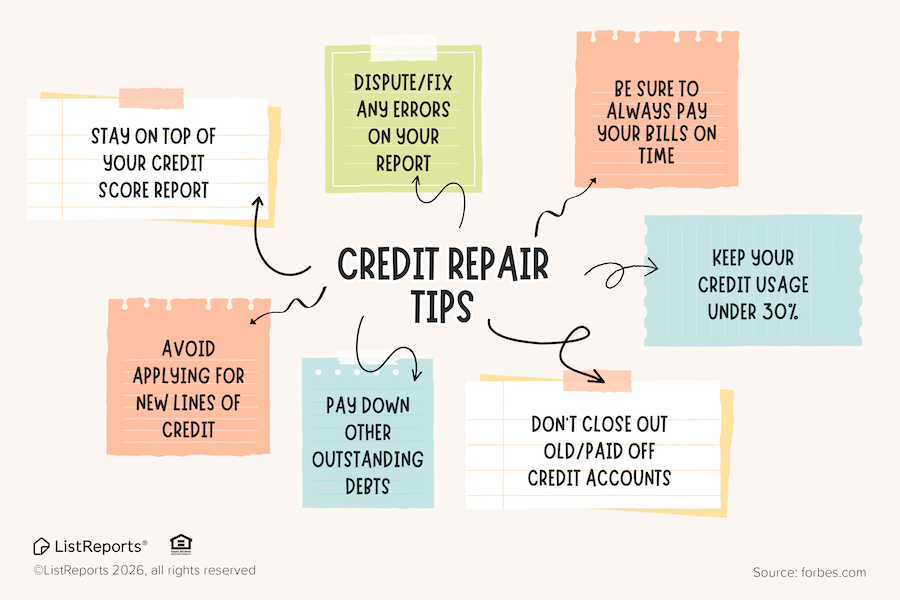

The plan might involve paying certain credit card balances down to targeted utilization levels, reviewing which medical collections actually need attention, correcting reporting inaccuracies, and preserving positive trade lines instead of closing accounts.

The difference here is subtle but important.

The goal is not necessarily to reduce debt as quickly as possible. The goal is to improve mortgage eligibility and credit scoring efficiency.

Within a few months, the couple may see meaningful score increases simply by lowering utilization and adjusting how accounts are reported. A score increase from 620 to even the mid-600s can open up significantly better financing options, lower mortgage insurance costs, and improve monthly affordability.

In many cases, this path creates a faster route to mortgage approval because the strategy is specifically built around how mortgage underwriting works.

⚖️ Why This Matters for Buyers

This is the part many people never hear in the commercials.

Financial programs are often designed with different end goals in mind.

A debt consolidation company may prioritize reducing monthly obligations and resolving long-term debt. A credit optimization strategy may prioritize improving mortgage qualification as quickly and efficiently as possible.

Neither approach is automatically right or wrong. It depends entirely on the borrower’s goals and timeline.

If someone is years away from buying and simply needs breathing room financially, consolidation may make perfect sense. But if someone hopes to buy within the next six to twelve months, the wrong program could unintentionally delay that process.

That’s why it’s so important to talk with a mortgage professional before enrolling in any debt or credit program.

Because sometimes the solution that sounds the most helpful today may not line up with the financial goal you have tomorrow.

☕ Final Thoughts

Buying a home is not just about having less debt. It’s about understanding how lenders evaluate your entire financial picture.

The right strategy can help improve scores, increase buying power, and create more options. The wrong strategy can unintentionally slow the process down.

Before signing up for a debt settlement, consolidation, or credit repair program, make sure you understand how it could affect your mortgage timeline and approval options.

A little planning upfront can save months of frustration later.

🎯If you’re thinking about buying a home or refinancing and aren’t sure where to start, let’s build a plan that supports both your financial goals and your homeownership goals.