March 31, 2026

📉 Why Rates Improved

Mortgage rates moved lower for the second straight day as markets responded to headlines suggesting the Iran war may be moving toward de-escalation.

Overnight, bonds improved after comments from President Trump suggested the conflict could potentially end, even if the Strait of Hormuz had not yet reopened. That matters because the Strait is a major shipping route for global oil, and anything that disrupts it tends to rattle markets quickly.

Later in the day, rates improved even more after reports surfaced that Iranian officials were “ready to end the war.” Markets liked the headline — but not enough to throw a party. Why? Because those comments reportedly came with conditions, including requests for “certain guarantees,” and they came from Iran’s President rather than the Supreme Leader. In market terms, that translates to: encouraging, but not exactly carved in stone.

🏦 What This Means for Mortgage Rates

Mortgage rates are heavily influenced by the bond market — especially mortgage-backed securities and U.S. Treasuries. When investors get nervous, they often move money into bonds for safety. That pushes bond prices higher and yields lower, which can help mortgage rates improve.

That’s exactly what happened here.

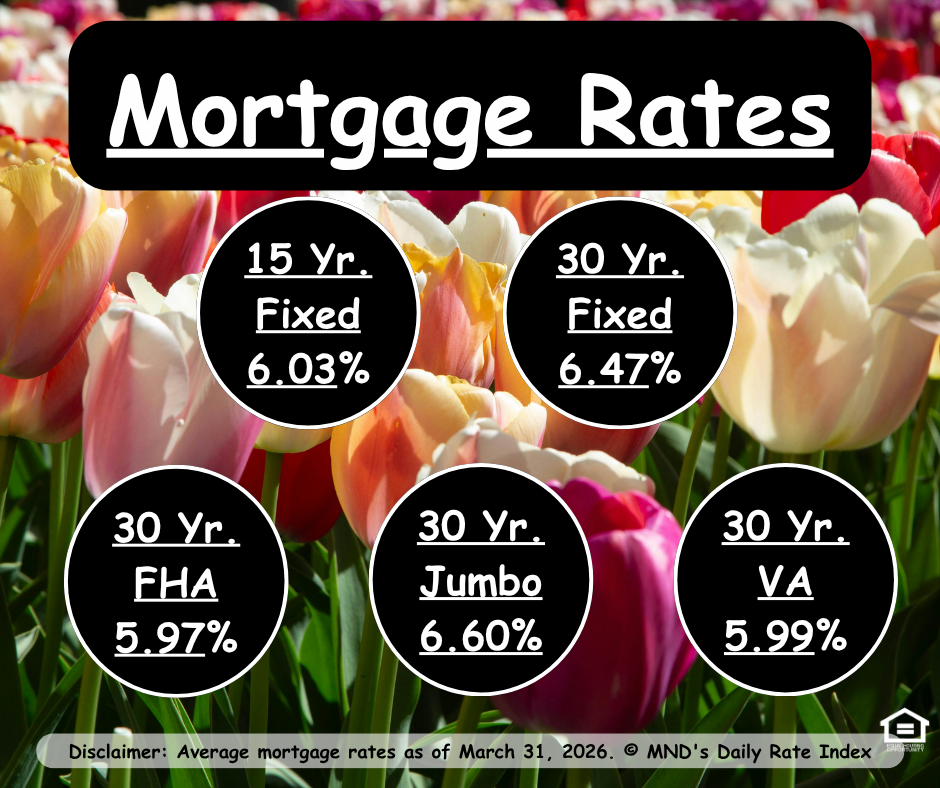

As stocks, oil, and bond markets all reacted to the possibility of easing tensions, bonds gained strength and lenders were able to price loans a little more favorably. The net effect was that average top-tier 30-year fixed mortgage rates moved back below 6.50%.

That’s a welcome shift after a pretty ugly run-up in rates over the past several days.

⚠️ The Catch Nobody Should Ignore

Before anyone starts popping champagne and locking loans in interpretive dance, there’s an important caveat:

Big improvements often happen right after rates have recently spiked to higher levels.

In other words, yes — this is good news. But it’s also partly the market correcting after a sharp move upward. That doesn’t necessarily mean we’re entering a long, smooth downward trend from here.

Markets are still highly sensitive to every new headline, and with geopolitical developments changing by the hour, rate volatility is still very much alive and well. This is not yet a “rates are back to normal” moment. It’s more of a “the fire alarm stopped for now” moment.

🏡 Why This Matters for Buyers and Homeowners

Even small movements in rates can have a real impact on affordability, payment comfort, and overall loan strategy.

For buyers, this kind of improvement may create a better opportunity to lock if they’re under contract or getting close to making an offer.

For homeowners watching the market for refinance opportunities, it’s another reminder that timing matters — and that market shifts can happen quickly, especially when rates are being driven by global news rather than just economic data.

This is also a great example of why trying to “perfectly time the bottom” can be a risky game. The market loves chaos and hates certainty. Very rude of it, honestly.

🐼 The Bottom Line

Rates finally gave us a little relief, and that’s good news — but the market is still walking on eggshells.

If you’re actively shopping, under contract, or wondering whether now is a smart time to lock or refinance, this is the kind of environment where strategy matters more than ever.

Have questions about what today’s market means for your payment, buying power, or next move? Reach out — I’m always happy to help you make sense of the madness.