March 24, 2024

Mortgage rates moved higher again today, and the culprit was not your average boring economic report.

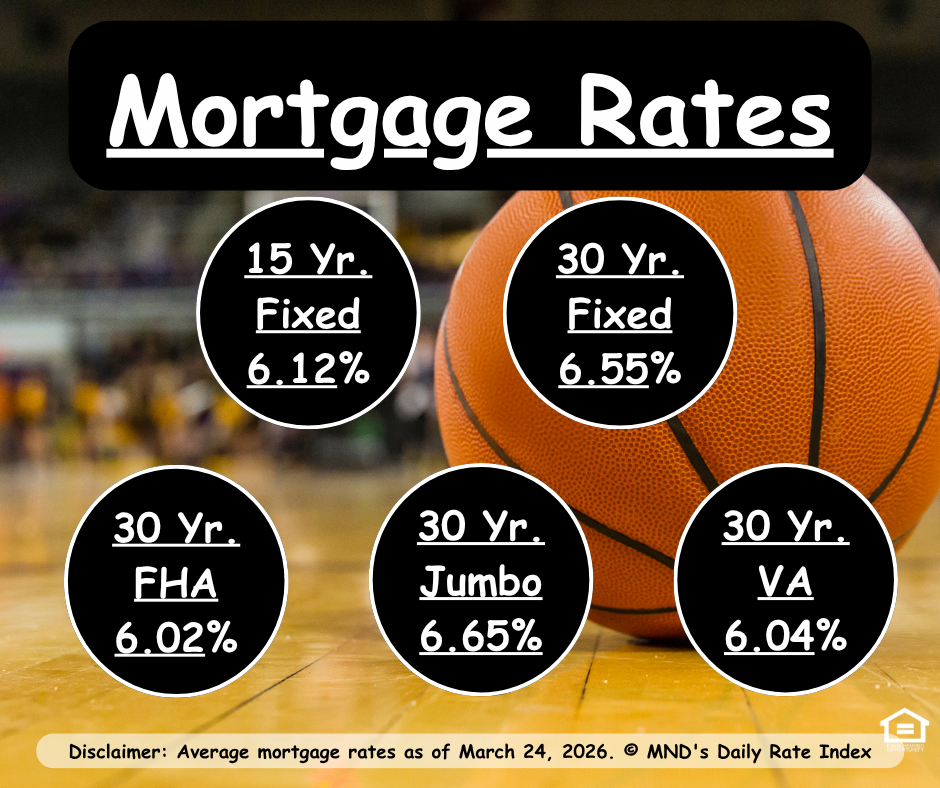

The bond market reacted sharply after midday headlines regarding possible U.S. troop deployment added new uncertainty to an already tense geopolitical environment. That pushed mortgage pricing worse during the afternoon, and many lenders repriced for the worse after the market selloff. As of today, the average top-tier 30-year fixed mortgage rate hit 6.55%, the highest level we’ve seen since August 2025.

In classic market fashion, later comments hinting at de-escalation helped bonds recover some of the initial damage. But not enough to fully undo the day’s pain.

Translation: the market had a brief panic attack, then decided to only partially calm down.

⚠️ Why the Iran Conflict Still Matters for Rates

At this point, mortgage rates are not just reacting to headlines—they’re reacting to what those headlines could mean next.

The big issue is energy. When war or geopolitical instability threatens oil supply, energy prices tend to rise. And when energy prices rise, inflation concerns tend to follow. That matters because mortgage rates are heavily influenced by the bond market, and bonds are very sensitive to inflation risk.

So even if the war ended tomorrow, rates likely would not simply snap back to where they were in February. That’s because markets are already trying to price in the aftershocks, not just the event itself.

And yes, markets love to overreact first and sort out the details later. Very mature behavior.

🛢️ What Are “Second Round Effects”?

This is one of those economist phrases that sounds way more dramatic than it needs to.

Second round effects happen when higher energy prices don’t just affect gas at the pump or your electric bill—but start working their way into the broader economy. Think:

higher shipping costs

higher production costs

higher prices for goods and services

more inflation expectations baked into consumer and business behavior

The Federal Reserve has noted that oil price spikes can create gradual but meaningful inflation pressure over time, not just immediately. In other words, the concern is not only “oil is more expensive today,” but also “what else gets more expensive next?”

That’s why markets are still uneasy. Even if the immediate military headlines cool off, the economic ripple effects may not.

🏡 What This Means for Buyers and Homeowners

For buyers, today is a good reminder that mortgage rates can move fast when global events hit the market.

A lot of people assume rates only change because of the Fed, inflation reports, or jobs data. Those absolutely matter—but so do geopolitical shocks, energy disruptions, and anything that can change investor sentiment in a hurry.

That means:

locking strategically matters

waiting can help… or backfire

timing the market perfectly is still mostly fiction

If you’re actively shopping, under contract, or thinking about refinancing, this is the kind of market where having a plan matters more than trying to guess the next headline.

Because yes, your mortgage strategy should ideally be based on more than “well, I saw something weird on Twitter.”

👀 My Take

Right now, the market is looking for something more definitive before it meaningfully improves pricing.

A vague hopeful headline can help for a few hours, but bonds and mortgage rates will likely stay jumpy until there’s a more credible and durable sign of de-escalation. Until then, volatility is still very much invited to the party.

If you have a buyer who’s on the fence, this is a good time to remind them:

you do not need perfect rates to make a smart move—you need a smart plan.

And that part? I can help with.

📞 Let’s Talk Strategy

If you or your clients are wondering whether now is the right time to lock, buy, refinance, or just game-plan the next move, I’m happy to walk through it.

Sometimes the best thing in a chaotic market is just having someone translate the nonsense into an actual strategy.