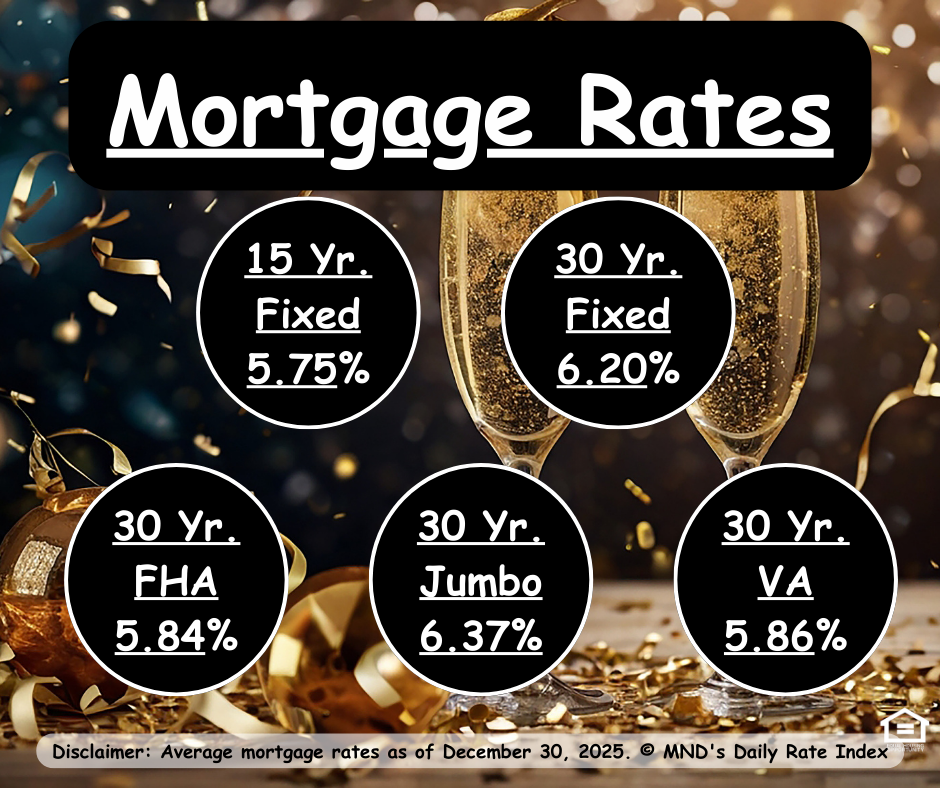

December 30, 2025

Mortgage rates spent the final full week of 2025 doing… not much. And honestly? That’s not a bad thing.

Rates moved sideways, staying within the same narrow range we’ve seen for most of Q4

Bond markets were quiet and thinly traded due to the holidays

No major economic data releases to push rates meaningfully higher or lower

Lenders largely held pricing steady, with only minor day-to-day adjustments

In short: calm, boring, and predictable — the financial equivalent of sweatpants between Christmas and New Year’s.

Why That Matters

Stability matters. After the volatility of the last few years, a steady rate environment gives buyers, sellers, and homeowners something we haven’t had much of lately: room to plan.

This stretch of consistency suggests:

Inflation fears are cooling, even if not gone

Markets are waiting for confirmation, not panicking

Rate spikes don’t appear imminent heading into early January

Looking Ahead to 2026

As we roll into the new year, expectations are cautiously optimistic — not for dramatic drops, but for gradual improvement.

Here’s what we’re watching:

Key economic data returns in early January (jobs, inflation, consumer spending)

Markets are increasingly focused on when, not if, rates ease further

Most forecasts point to slow, uneven declines, not a straight line down

Translation: 2026 is shaping up to be a year where strategy beats timing. Preparation, flexibility, and smart loan structuring will matter more than waiting for a magic rate.

Quick Takeaway

Rates ended 2025 steady and uneventful — and that’s actually a strong setup for 2026. If you’re planning to buy, refinance, or just want to understand your options, this is a solid moment to get informed and be ready.

Want to run numbers, explore scenarios, or map out a 2026 plan? Let’s taco ’bout it 🌮