Inflation Persists: What February's Economic Data Means for Mortgage Rates and Home Buyers

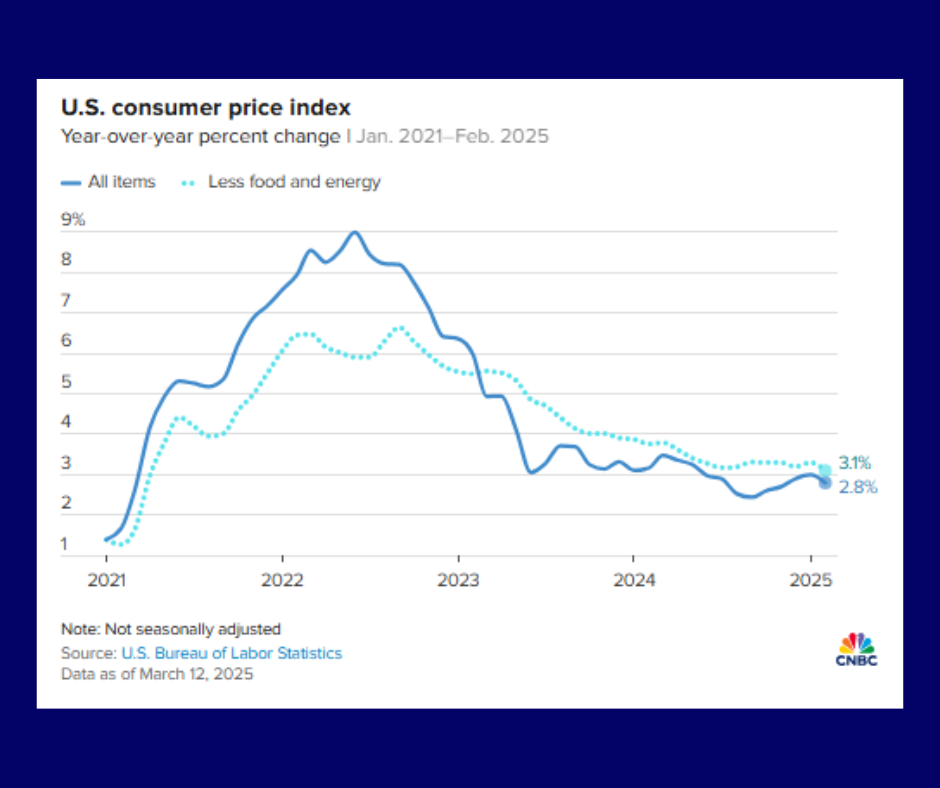

The February report from the Commerce Department shows that inflation remains persistent but not alarmingly high, with the core personal consumption expenditures (PCE) price index rising 0.4% in February, slightly above expectations. The inflation rate for the year stands at 2.8%. However, consumer spending increased at a slower-than-expected pace (0.4%), and personal income rose 0.8%. This data suggests a stable economy, but with some caution among consumers due to higher prices in certain sectors.

The Federal Reserve monitors the PCE index closely, as it is seen as a better gauge of long-term inflation trends. The report indicates that inflation is still above the Fed’s target, but not enough to push them into quick action on interest rates. While inflation isn't surging, concerns about potential tariffs and trade wars could add upward pressure on prices, which may keep the Fed in a "wait-and-see" mode regarding rate cuts.

What does this mean for mortgage rates, home buyers, and sellers?

Mortgage Rates: The Federal Reserve is unlikely to cut interest rates in the short term due to the ongoing inflation concerns. This means mortgage rates may remain relatively high or even increase slightly as the Fed continues to watch economic data. Buyers should expect rates to stay in the current range, with slight fluctuations based on broader economic news.

Home Buyers: Higher inflation, paired with steady consumer spending and income growth, suggests that home buyers may face higher borrowing costs in the near future. Buyers looking to lock in lower rates may want to act sooner rather than later, especially as inflation pressures could lead to rate hikes or prolonged elevated rates.

Home Sellers: For sellers, the current economic conditions mean that the market remains stable, but there may be a slowdown in activity if mortgage rates rise or remain high. Sellers may need to be prepared for slightly less urgency from buyers and could benefit from pricing strategies that account for higher borrowing costs.

In summary, while inflation and spending data point to a stable economy, the Fed’s cautious stance on rate cuts means mortgage rates are likely to remain steady or even increase, which could influence buyer demand and overall market activity.

If you're considering buying or refinancing, now may be a good time to lock in a mortgage rate before potential rate increases. With inflation still a concern and the Fed's cautious approach, rates could rise or remain steady in the coming months. Don’t wait—reach out today to explore your mortgage options and secure a competitive rate