What’s Really Driving Mortgage Deals Right Now

🧭 The Shift Happening Beneath the Surface

If you only watch mortgage rates, you’re missing half the story.

Yes, rates still matter — but the biggest changes I’m seeing come from how transactions are structured and managed from day one. As inventory gradually improves and buyers adapt to the current environment, strategy is becoming more important than timing.

Key shifts happening right now:

Buyers taking a more strategic approach rather than rushing

Sellers prioritizing certainty and strong financing over just price

Increased collaboration between agents and lenders to reduce risk upfront

🏡 Negotiation Leverage Is Quietly Changing

Compared to the ultra-competitive markets of recent years:

Contingencies are becoming more acceptable again

Seller concessions are appearing more frequently

Financing strategy is playing a larger role in offer strength

This creates opportunities for buyers — but only if they’re properly prepared.

🤝 A Strategy I’m Seeing More Often (And Loving)

One of the most interesting trends I’m seeing is seller’s agents requesting that buyers get prequalified with their preferred lender — often me — when their client is selling a home while simultaneously purchasing another.

At first glance, this might sound redundant, but it’s actually a brilliant risk-management strategy.

When a seller is relying on their home sale to fund their next purchase, loan issues on the buyer’s side can derail everything. By having buyers complete a thorough prequalification with a trusted lender:

Potential underwriting issues are identified early

Loan contingencies become more reliable

Sellers gain peace of mind that the transaction won’t fall apart unexpectedly

It introduces more control into what can feel like a scary and uncertain process.

And honestly — it’s a win-win.

It gives me the opportunity to step in, review the scenario thoroughly, and sometimes “wow” another buyer with clarity and strategy — while making the referring agent look like a rockstar for keeping the transaction on the right track.

💼 Strategy Is Outperforming Timing

Many buyers still believe they need to wait for perfect conditions. What I’m seeing tells a different story.

The strongest outcomes are coming from clients who:

Prepare financially before shopping

Focus on payment strategy instead of just rate headlines

Align financing early with their offer strategy

I always aim to uncover potential issues before clients start house hunting. That preparation reduces stress and helps create smoother transactions from contract to closing.

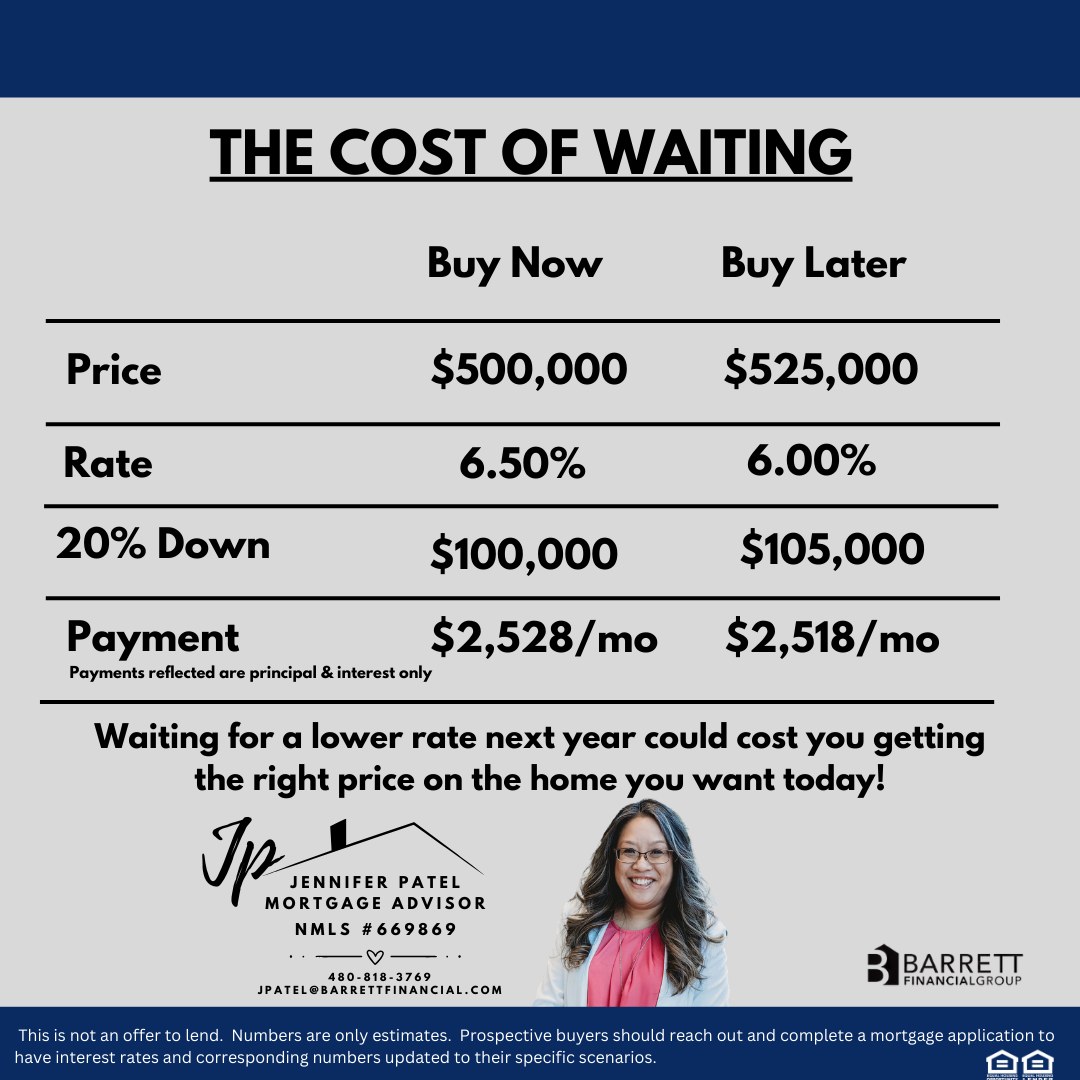

⏳ The Cost of Waiting

Another conversation I’m having more frequently is about the cost of waiting.

Yes — rates may go down over time. But historically, when rates improve meaningfully, more buyers quickly jump back into the market. Increased demand often brings stronger competition, fewer concessions, and upward pressure on home prices. In other words, lower rates don’t always mean an easier buying environment.

What that means in real life:

A slightly lower interest rate can be offset by higher purchase prices driven by increased competition.

Buyers who wait for perfect timing may lose negotiating leverage that exists today.

Entering the market when competition is more balanced can sometimes create better long-term positioning.

The buyers who feel most confident right now aren’t trying to predict the perfect moment — they’re focusing on controlling what they can control: purchase price, negotiation strength, and overall strategy. While no one can guarantee where rates will go next, refinancing later is always a possibility if the market improves. What buyers can’t do is go back in time to capture yesterday’s price or today’s negotiating opportunities.

📈 Buyer Psychology Is Evolving

Another shift I’m seeing is buyers becoming more analytical and intentional about their decisions. Instead of reacting emotionally to headlines, many are stepping back and asking smarter long-term questions.

One conversation that comes up frequently is the rent versus buy comparison — especially when buyers feel stuck waiting for the “perfect” market conditions.

Let’s look at a real-world perspective.

A monthly rent payment of $2,500 over the past three years adds up to roughly $90,000 paid toward housing. That’s a significant amount — and it naturally leads to an important question:

What could that $90,000 have done if it had been applied toward homeownership?

Depending on the scenario, it could have contributed toward:

Building equity through principal reduction

Benefiting from potential appreciation

Creating leverage for future moves or financial goals

Of course, renting can absolutely make sense in certain situations, and buying isn’t always the right answer for everyone. But more buyers are starting to evaluate not just the monthly payment — but the long-term impact of where their housing dollars are going.

This shift in mindset is helping clients make more intentional decisions, focusing less on trying to perfectly time the market and more on aligning their housing choices with their overall financial strategy.

🧠 What This Means Going Forward

If these trends continue, we’ll likely see:

Increased collaboration between agents and lenders early in the process

More emphasis on prequalification depth and accuracy

Creative strategies that reduce uncertainty for both buyers and sellers

The real advantage today isn’t just rate — it’s preparation and partnership.

🙋 Have Questions? Let’s Talk.

Every transaction is different, and sometimes a quick conversation can make all the difference in preventing surprises later. If you have questions about strategy, prequalification, or how to keep your next deal on track, reach out to me anytime — I’m always happy to help you map out the smartest path forward.

📚 Sources

Mortgage News Daily – Market rate trends and bond market commentary

National Association of Realtors – Existing home sales and inventory trends

FHFA Housing Data – Housing market indicators and pricing trends