PMI Made Simple

What Is Private Mortgage Insurance (PMI)?

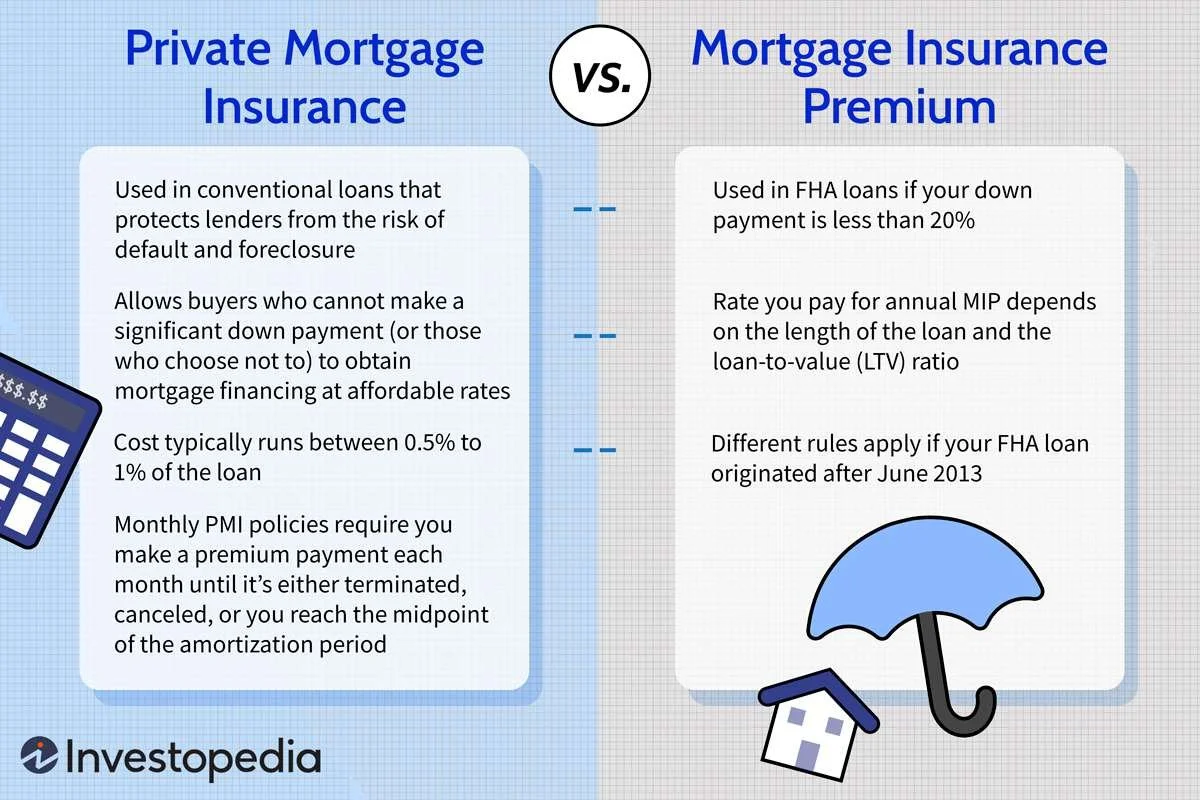

Private Mortgage Insurance (PMI) is insurance that protects the lender, not the borrower, when a buyer puts down less than 20% on a home purchase using a conventional loan.

Let’s be clear: it doesn’t insure your house. It doesn’t protect your equity. It simply reduces the lender’s risk when you bring a smaller down payment to the table.

So why does it exist? Because PMI allows buyers to purchase sooner instead of waiting years to save 20% down. And in many markets, that timing can matter more than the insurance cost itself.

💡 Why Is PMI Relevant to Mortgage Loans?

PMI plays a big role in affordability strategy.

Without it, lenders would require 20% down on nearly every conventional loan. PMI creates flexibility. It allows:

First-time buyers to enter the market sooner

Move-up buyers to retain cash for renovations or reserves

Investors (on some conventional products) to leverage capital strategically

In short, PMI is the trade-off for a lower down payment.

📋 What Loan Types Require PMI — And Which Don’t?

Here’s where things get important:

Loans That Typically Require PMI:

Conventional loans with less than 20% down

Loans That Do NOT Use Traditional PMI:

FHA loans – These use mortgage insurance premiums (MIP), which follow different rules

VA loans – No monthly mortgage insurance

USDA loans – Have guarantee fees, but not PMI

Conventional loans with 20%+ down

If you’re using a conventional loan and putting down 5%, 10%, or 15%, PMI will apply in most cases.

🔓 How Do You Remove PMI After Closing?

This is the part everyone wants to know.

For conventional loans:

Automatic Removal

PMI must automatically terminate when your loan balance reaches 78% of the original home value (based on original amortization schedule)

Borrower-Requested Removal

You can request cancellation once you reach 80% loan-to-value (LTV)

You must be current on payments

The lender may require proof of property value (sometimes an appraisal)

Early Removal via Appreciation

If your home value increases significantly, you may be able to request removal earlier by:

Ordering an appraisal

Demonstrating sufficient equity

Now compare that to FHA loans:

If you put down less than 10%, FHA MIP typically stays for the life of the loan

With 10% down, it remains for 11 years

Big difference. Strategy matters.

💰 Can You Pay PMI Upfront Instead of Monthly?

Yes — and this is where smart structuring comes in.

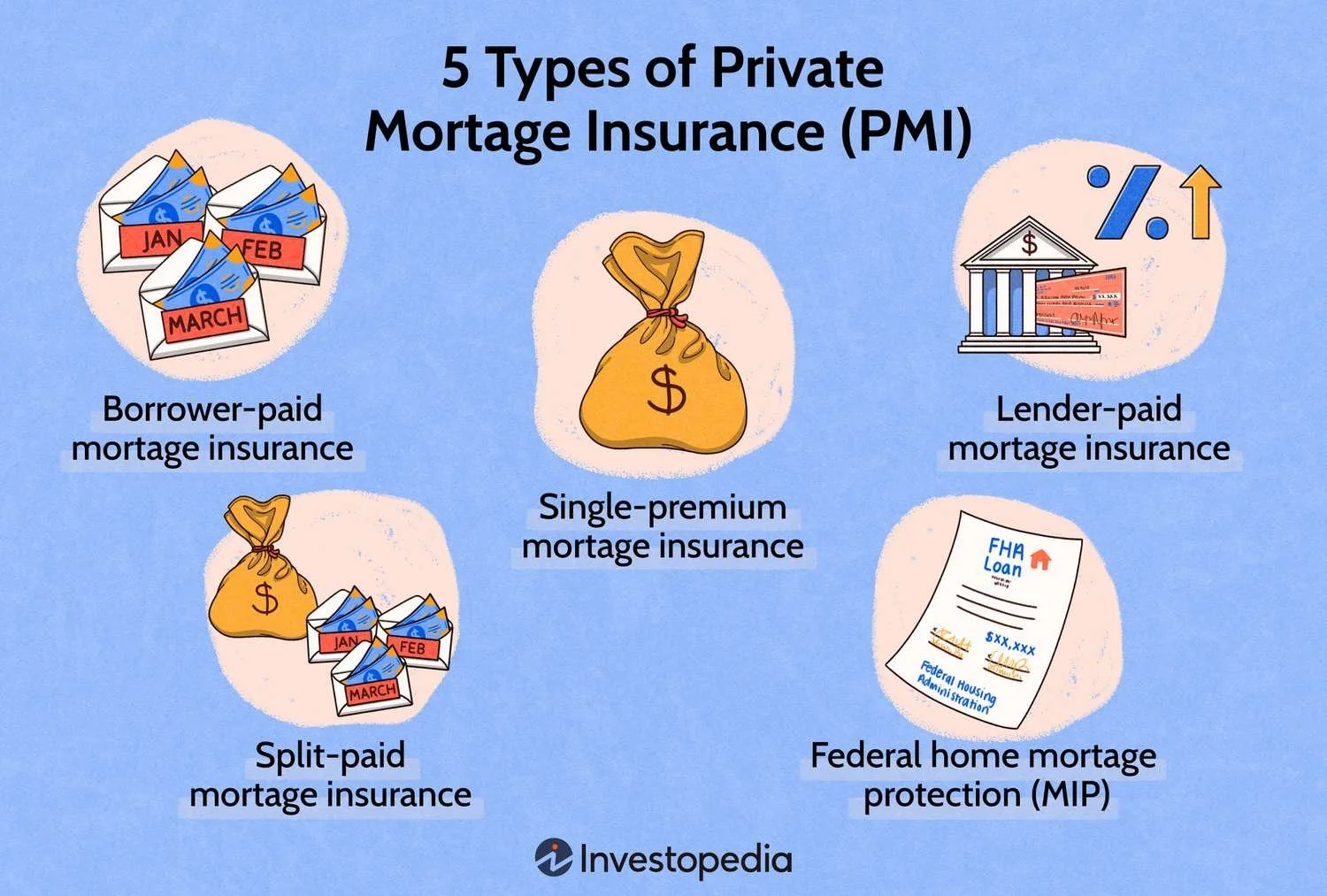

Conventional PMI payment options:

Monthly PMI – Most common; paid as part of your mortgage payment

Single-Premium PMI – Paid upfront at closing

Split Premium – Part upfront, part monthly

Lender-Paid Mortgage Insurance (LPMI) – Built into the interest rate

Each structure impacts payment, cash-to-close, and long-term cost differently.

⚖️ LPMI: Pros & Cons

LPMI means the lender covers the PMI cost — but in exchange, your interest rate is slightly higher.

Pros:

No separate monthly PMI line item

Cleaner payment structure

May be helpful if you plan to keep the loan short-term

Cons:

Higher interest rate for the life of the loan

Not removable like traditional PMI

Could cost more long-term if you keep the loan many years

In some scenarios, LPMI makes sense. In others, traditional monthly PMI that can later be removed is smarter.

It’s not about “avoiding PMI.” It’s about structuring it intentionally.

📊 Quick Reference Summary

PMI applies to conventional loans under 20% down

It protects the lender, not the borrower

It can be removed at 80% LTV (by request) or 78% (automatic)

FHA, VA, and USDA follow different insurance rules

You can choose monthly, upfront, split, or lender-paid options

LPMI trades a higher rate for no separate PMI payment

🐼 Final Thought

PMI is not a punishment. It’s a tool.

The right strategy depends on:

How long you plan to keep the home

Your cash position

Your risk tolerance

Market appreciation trends

There is no one-size-fits-all answer — and that’s where strategy comes in.

🔥If you’re buying, refinancing, or just trying to understand your options, give me a call. I’m happy to run scenarios and walk through the numbers with you.