May 19, 2026

It was another bruising day for the bond market, and mortgage rates definitely felt it.

Investors came out swinging early this morning, aggressively selling off bonds during the first two hours of trading. That pushed the 10-year Treasury yield to its highest level in more than a year — and when Treasury yields climb, mortgage rates usually follow right behind.

The good news? Mortgage-backed securities (the bonds tied directly to home loans) have actually been holding up better than Treasuries over the past several months. Increased purchasing activity from Fannie Mae and Freddie Mac has helped soften some of the upward pressure on rates.

In plain English: mortgage rates could be even worse right now.

But even with that support, rates are still climbing.

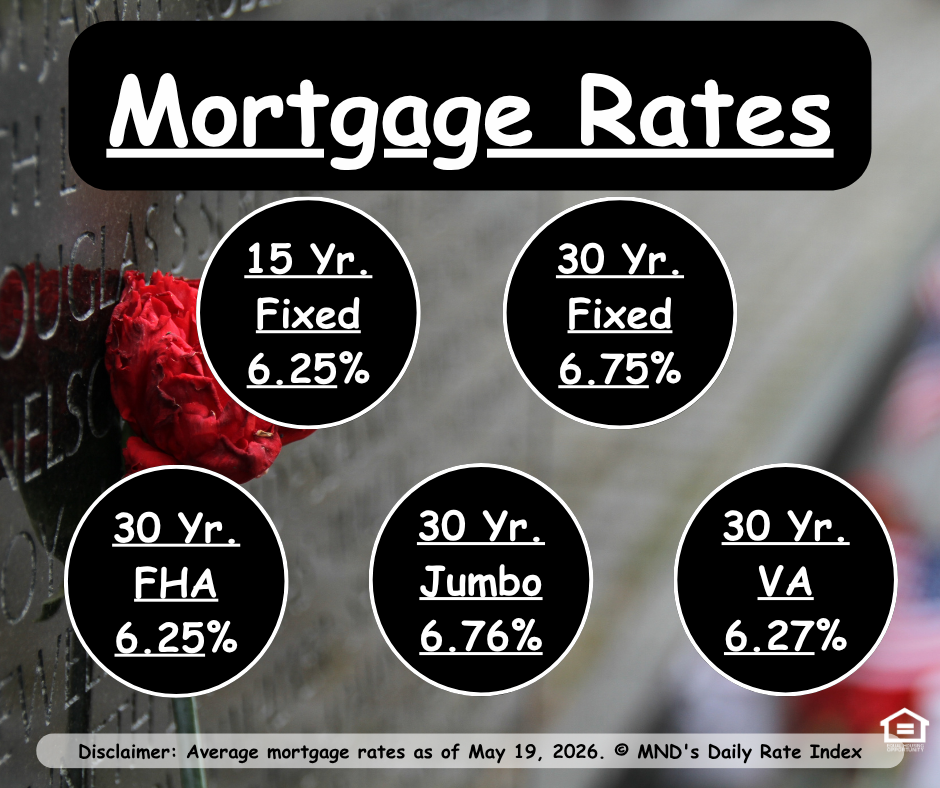

Today’s average top-tier 30-year fixed mortgage rate reached approximately 6.75%, the highest level we’ve seen since July 2025. Even more eye-opening? Rates are now roughly 0.75% higher than they were before the Iran conflict began impacting global markets.

That makes this one of the fastest mortgage rate spikes we’ve seen since late 2024.

📈 Why Are Rates Moving So Fast?

Several factors are colliding all at once:

Ongoing geopolitical uncertainty

Inflation concerns lingering in the market

Investors pulling money out of bonds

Stronger economic data reducing expectations for aggressive Fed cuts

When investors sell bonds, bond prices fall and yields rise. Mortgage rates are heavily influenced by those bond yields — especially the 10-year Treasury.

While the Federal Reserve doesn’t directly set mortgage rates, the market’s expectations around inflation, economic growth, and future Fed policy heavily influence where rates go next.

🏡 What This Means for Buyers and Homeowners

A sudden rate jump can absolutely affect affordability. Monthly payments rise quickly when rates move this sharply in a short period of time.

But here’s the important part:

People are still buying homes.

Why? Because buyers are adapting. They’re negotiating more aggressively, asking for seller concessions, utilizing temporary buydowns, and exploring creative financing strategies that simply weren’t available during the frenzy markets of the past few years.

In many markets, homes are sitting longer, competition has cooled, and buyers finally have room to negotiate again.

That creates opportunity — even in a higher-rate environment.

🐼 Mortgage Minute Takeaway

The headlines may sound dramatic, but strategy matters more than panic.

Markets move. Rates fluctuate. But families still need homes, investors still buy property, and smart planning still wins.

If you’re wondering how today’s rate environment affects your buying power, refinance options, or long-term plans, let’s build a game plan that works for your situation instead of letting the news cycle make the decisions for you.