February 10, 2026

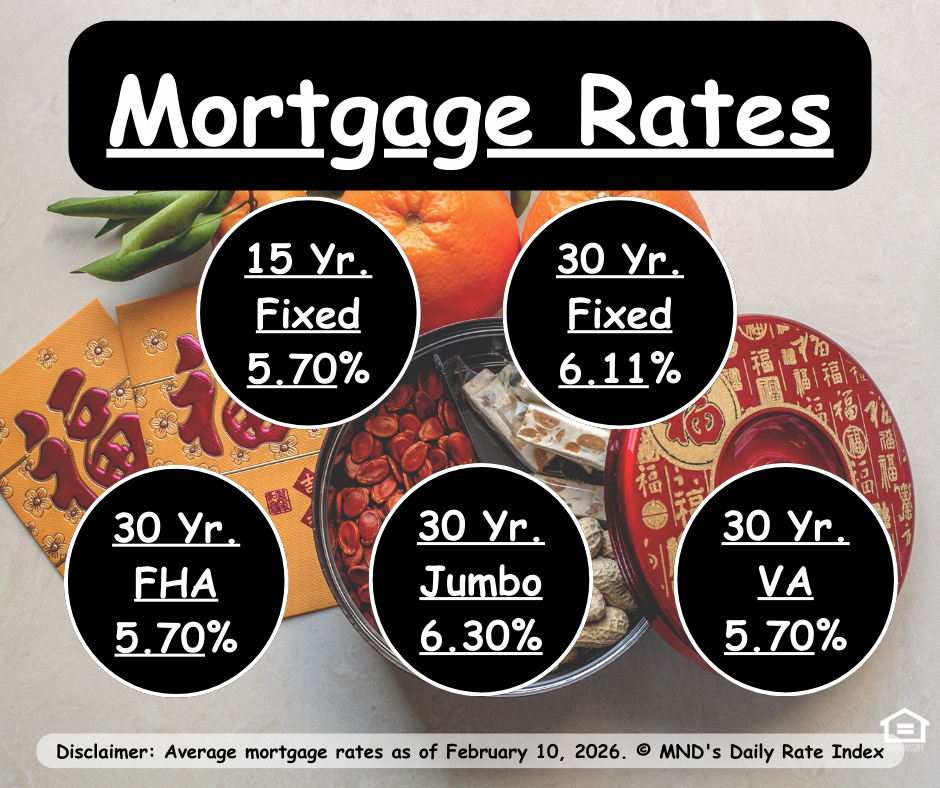

Mortgage rates moved lower Tuesday following a weaker-than-expected Retail Sales report, pushing the average 30-year fixed rate to approximately 6.11% — the largest single-day improvement since early January and a clear break below the recent narrow range of 6.15%–6.20%.

Instead of slowing down after recent gains, bond markets kicked the rally into higher gear. Rather than circling the wagons and consolidating, investors increased buying activity, driven by surprisingly soft consumer spending data.

📊 What Drove the Move?

Mortgage rates follow the bond market, and bonds react quickly to economic signals.

Here’s the key dynamic:

📉 Weak economic data tends to support lower rates.

📈 Strong economic data can push rates higher.

The latest Retail Sales report added to a growing list of softer economic indicators that are encouraging markets to position for a potentially weaker jobs report. That anticipation has helped fuel a stronger rally in bonds — translating into improved mortgage pricing.

In fact, rates have improved by nearly 15 basis points in less than a week, which is a meaningful shift in a relatively short period.

👀 Why Tomorrow’s Jobs Report Matters So Much

The employment report remains the most influential recurring economic release for interest rates, and the market appears to be leaning toward expectations of softer labor data.

But here’s where things get interesting:

If the jobs report comes in especially weak, the current rate rally could continue.

If the data surprises to the upside, bonds could face a reasonably brisk correction — meaning mortgage rates could move higher again.

As always, the degree of volatility will depend on how far the actual data deviates from expectations.

🧭 What This Means for Buyers and Homeowners

This week is a perfect reminder that rate movements are often driven by economic momentum rather than headlines alone.

Key takeaways:

Rates can improve quickly when markets anticipate slower economic growth.

Rapid improvements can also increase the risk of short-term pullbacks.

Timing the market perfectly remains difficult — strategy matters more than guessing the next data point.

For buyers, improved rates may increase affordability. For homeowners, dips like this can create windows of opportunity worth evaluating.

☎️ Final Thoughts

Mortgage rates are benefiting from a strong bond rally, but the next move likely hinges on tomorrow’s jobs report. The market is positioned for potential weakness — which means surprises in either direction could trigger volatility.

Call me with questions — I’m always here to help you understand what today’s rate movement means for your next step.